Title Insurance Colorado – Expert Protection 2026

Title insurance protects Colorado property buyers from hidden legal claims that could surface after closing. Unlike homeowner’s insurance that guards against future damage, it safeguards against past title defects like undisclosed liens, boundary disputes, or fraudulent signatures. When you’re buying a home in Colorado, understanding this protection ensures your investment stays secure for decades.

TL;DR

Title Insurance Colorado protects buyers and lenders from ownership disputes tied to a property’s past. Owner’s policies cover your equity lifelong, while lender’s policies protect mortgage interests until loan payoff. Costs typically range $1,000–$2,000 based on purchase price, with sellers often covering the owner’s policy in most transactions. The process involves a title search, clearing any issues, and issuing your policy at closing. Shopping among licensed Colorado title companies saves money and ensures thorough protection. The title insurance industry paid $676 million in claims nationally in 2024, reflecting the real financial risks this coverage prevents. This guide breaks down title insurance Colorado buyers and sellers see at closing, including what it covers, what it costs, and how to avoid delays.

Key Points

- Owner’s title insurance protects your equity; lender’s title insurance protects the mortgage company

- Average costs: 0.5%–1% of purchase price, or roughly $1,000–$2,000 for median Colorado homes

- Sellers typically pay owner’s policy; buyers pay lender’s policy

- Title searches take 1–3 weeks, with full process completing by closing day

- Coverage includes liens, fraud, boundary errors, and undisclosed heirs

- Request quotes from multiple licensed Colorado title companies to compare total fees

Table of Contents

What Title Insurance Is and Why Colorado Property Buyers Need It

Title insurance is a one-time premium that protects your property ownership from legal claims rooted in past title defects. It covers issues like unpaid liens, forged documents, or undisclosed heirs that could challenge your rights years after purchase.

Colorado buyers face unique risks that make this protection particularly valuable. Take a Boulder County property where a $38,000 mechanic’s lien from a 2019 renovation surfaced three days before closing. The title company cleared the lien through the seller, and the buyer’s policy prevented any residual claims. This avoided potential litigation costs exceeding $15,000. Without title insurance, the new owner could have inherited both the lien and the legal battle.

Water rights disputes create another common scenario. In ski resort communities, a buyer might discover that previous owners sold recreational water rights to a homeowners association, limiting their property’s future use options. Mineral rights issues prove equally complex in Colorado’s Front Range and Western Slope regions, where severed subsurface rights give others legal access to extract resources beneath your land.

A thorough title search identifies most problems before closing, but some defects only surface later. Title insurance pays legal defense costs and financial losses if covered claims arise, protecting the equity you’ve worked hard to build.

At JROC Properties, we help buyers avoid closing-day surprises, and title insurance is one of the most misunderstood line items. If you’re early in the process, grab our Buyer’s Guide to understand the full closing checklist.

How Title Insurance Differs From Other Property Insurance

Standard property insurance covers future events like fire or storm damage through recurring premiums. Title insurance works backward, protecting against past events already recorded or hidden in property history before you owned the home.

Traditional insurance reimburses losses after incidents occur. Title insurance prevents losses through upfront title searches that clear issues before closing. If a defect slips through, your policy covers legal fees and ownership disputes without ongoing premiums. You pay once at closing and get lifelong coverage.

This makes title insurance unique. Homeowner’s insurance protects your structure; title insurance protects your legal right to own that structure. Both matter, but they cover completely different risk categories.

Common Title Issues That Threaten Colorado Property Ownership

Unpaid liens create the most frequent title problems. Previous owners may have left unpaid contractor bills, HOA dues, or tax assessments attached to the property. These liens transfer with the deed, making you responsible unless cleared before closing. Average closing costs in Colorado include title search fees precisely to uncover these hidden debts.

Boundary disputes cost homeowners thousands in legal fees when neighbors’ fences encroach onto property lines or old surveys mismarked boundaries. For a $500,000 Denver home with a fence encroachment of 3 feet onto your property line, resolving this issue could cost $8,000–$15,000 in legal fees and new surveys. That makes a survey endorsement’s $250 premium a clear value proposition.

Recording errors in county clerk offices can misidentify owners or incorrectly list easements. Forgery, fraud, and undisclosed heirs pose equally serious threats. A forged signature on a past deed or an unknown heir claiming inheritance rights can invalidate your purchase, creating expensive legal battles that title insurance covers.

Types of Title Insurance Coverage in Colorado

Two distinct policies protect different parties in real estate transactions. Understanding both ensures complete coverage for your specific role.

Owner’s Title Insurance Policy

Owner’s title insurance protects your equity investment for as long as you own the property. It covers claims against your ownership, including fraud, liens, boundary disputes, and undisclosed heirs. If someone challenges your title, the policy pays legal defense costs and financial losses up to the full purchase price.

This coverage never expires and transfers to your heirs. You pay a one-time premium at closing, typically 0.5% to 1% of the purchase price. For Colorado’s median home price, that translates to roughly $1,000–$2,000.

Colorado custom traditionally assigns owner’s policy costs to sellers, though this remains negotiable in your purchase contract. Owner’s policies are optional but strongly recommended since lender’s policies protect only the mortgage company, not your equity.

Lender’s Title Insurance Policy

Lender’s title insurance protects the mortgage company’s financial interest in your property. It covers the outstanding loan amount, decreasing as you pay down the mortgage. Banks require this policy for financed purchases to ensure their lien position stays secure against competing claims.

Buyers always pay lender’s policy premiums since it protects the lender. The cost typically runs lower than owner’s policies because coverage shrinks with the loan balance. If title defects surface, the lender’s policy may pay off the remaining mortgage, but you could still lose your down payment and equity without an owner’s policy.

This critical distinction surprises many first-time buyers. Both policies work together at closing, with simultaneous issue discounts often reducing combined costs by hundreds of dollars.

What Colorado Title Insurance Policies Cover and Exclude

Standard Colorado policies cover defective title claims, including hidden liens, forged documents, and errors in public records. Coverage extends to easements or rights of others not disclosed at purchase, undisclosed leases or contracts affecting the property, and survey-related encroachments discovered later. You receive legal defense for covered claims plus financial compensation if ownership is lost or impaired.

Exclusions limit coverage to pre-existing title problems only. Zoning violations, land use restrictions, and environmental hazards fall outside standard policies. Unrecorded claims not visible in public records typically aren’t covered unless discovered during the title search. Liens you create after purchase remain your responsibility.

Enhanced policies offer optional endorsements for broader protection. Colorado regulations require title companies to clearly disclose all proposed exceptions in your title commitment, helping you understand exact coverage limits before closing.

Coverage Category | Owner’s Policy | Lender’s Policy | Standard Exclusions |

Protects | Buyer’s equity | Lender’s loan amount | Future events (zoning, environment) |

Duration | Lifetime ownership | Until loan is paid off | Actions by insured owner |

Coverage Amount | Full purchase price | Decreasing loan balance | Known defects listed in exceptions |

Premium Timing | One-time at closing | One-time at closing | Matters discoverable by inspection |

Title Insurance Costs in Colorado: What to Expect

Understanding Colorado title insurance pricing helps you budget accurately for closing. Rates follow regulated structures, but total costs vary based on property value, type, and transaction complexity.

Average Title Insurance Rates for Colorado Properties

Colorado title insurance operates under regulated rate schedules filed with the Division of Insurance. Premiums typically range 0.5% to 1% of the property’s purchase price. For a $421,000 home, expect roughly $900–$1,400 in owner’s policy premiums before discounts. A $577,500 median-priced property runs approximately $1,400–$2,100.

Stewart Title’s 2025 rate filing shows basic premiums increasing by $9 for properties valued $0–$1 million in many urban areas. Minimums rose to $450 from $360 statewide. Geographic zones affect pricing, with mountain resort counties sometimes carrying higher rates due to complex title histories.

Short-term discounts dramatically reduce costs if your property had recent title insurance. Policies issued within the past 1–2 years qualify for 55% discounts off basic rates. Properties insured 3–5 years ago receive 70–75% off in most counties. These reissue savings can cut $400–$4,800 from your premium.

Lender’s policies add minimal expense when purchased simultaneously with owner’s policies. Most title companies bundle these for a small additional charge. Endorsements like boundary coverage or access protection cost $100–$1,000 extra depending on your property’s specific risks.

Factors That Affect Your Title Insurance Premium

Property value serves as the primary cost driver. Higher-priced homes pay higher premiums, though the per-thousand rate decreases as property value climbs. A $300,000 home might pay $3 per thousand, while a $1 million property pays closer to $2.50 per thousand in marginal costs.

Property type influences complexity and pricing. Residential properties follow standard rate schedules. Commercial properties often incur higher premiums due to coverage complexity and extensive lien searches. Vacant land may have different rate structures, especially if mineral or water rights create additional examination work.

Location within Colorado affects total costs. Urban counties with robust recording systems typically process title searches faster and more efficiently. Rural mountain counties may require extra research time to trace ownership histories through older, less digitized records, increasing service fees.

Transaction complexity adds variables. New construction requires extra endorsements for builder liens. Estate sales need additional work to verify heir interests. Properties with easements, rights-of-way, or HOA complications take longer to examine, increasing closing service charges beyond base insurance premiums.

Who Pays for Title Insurance in Colorado Transactions

Owner’s title insurance traditionally falls to sellers in most residential transactions across the Front Range and mountain communities. Sellers cover this as part of their roughly 2.45%–2.47% in closing costs. In title insurance Colorado transactions, contract language matters more than ‘rules,’ because most fees are negotiable.

Buyers almost always pay lender’s title insurance since it protects the mortgage company. This forms part of the buyer’s 2%–5% closing cost range and is required by mortgage lenders.

These customs remain fully negotiable. Your purchase contract’s Section 8 typically specifies who pays which title insurance costs. Strong seller’s markets may shift owner’s policy costs to buyers, while buyer’s markets often see sellers covering more expenses to close deals quickly.

The Title Insurance Process in Colorado

The title insurance process protects your transaction through systematic research, problem resolution, and policy issuance.

Title Search and Examination

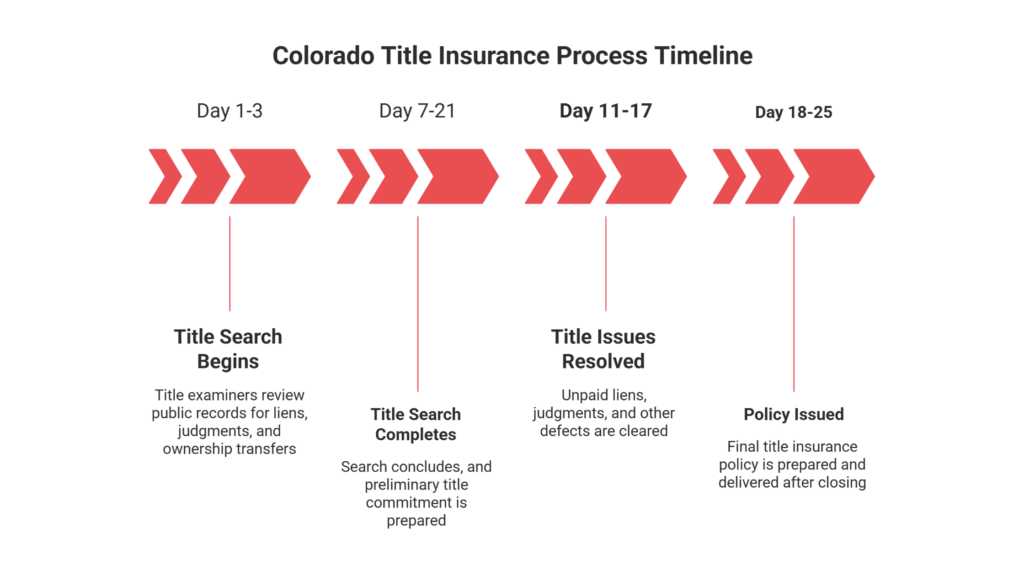

Title searches begin immediately when escrow opens, typically within 1–3 days of contract acceptance. Title examiners review public records at county clerk and recorder offices, searching for liens, judgments, easements, and ownership transfers dating back several decades.

Examiners verify legal descriptions, confirm current ownership, and check for unpaid property taxes or HOA dues. They review federal tax liens, divorce decrees, probate records, and bankruptcy filings that might affect the property. The search typically completes within a week for straightforward residential properties but may extend to three weeks for complex parcels.

The title company prepares a preliminary title commitment detailing their findings. This document lists the property’s legal description, current owner, required conditions for insuring, and specific exceptions to coverage. You receive this commitment early in the transaction, giving you time to review and address concerns.

Resolving Title Issues Before Closing

When the title search uncovers problems, the resolution phase begins. Common issues like unpaid liens or outstanding judgments must clear before the title company will insure. This takes 11–17 days on average, though complex problems may extend longer.

Title companies coordinate with creditors, attorneys, and county officials to release liens or correct recording errors. Sellers typically pay to clear title defects since they’re selling the property “free and clear.” If boundary disputes or easement conflicts surface, negotiations with neighbors or prior owners may be necessary.

Some issues require legal intervention. Forged documents, competing ownership claims, or missing heirs demand attorney involvement to establish clear title. Your title company manages these processes but may request extensions to your closing date if resolutions take longer than expected.

Colorado real estate contracts include standard contingencies for title clearing. These provisions protect buyers by allowing contract termination if title can’t be cleared within reasonable timeframes.

Issuing Your Title Insurance Policy

Final policy issuance happens after closing and recording. Once your deed records at the county, the title company prepares the formal title insurance policy reflecting your ownership. This process takes 18–25 days from initial title order through delivery.

The policy includes your property’s legal description, coverage amount, effective date, and detailed exceptions. Keep this document with your permanent property records. You’ll need it if filing future claims or when selling the property years later.

Colorado title companies must provide gap coverage notice before closing. This critical protection covers title matters that record between your closing time and when your deed officially records at the county. Without gap coverage, a lien filed during this window might not be covered under your policy.

Your policy remains active for your entire ownership period. If you discover covered defects years after purchase, file claims directly with the title insurance underwriter listed on your policy.

How to Choose a Title Insurance Company in Colorado

Selecting the right Colorado title insurance provider directly affects your transaction’s smoothness, cost, and long-term protection.

Top 3 Factors for Choosing Your Colorado Title Insurance Provider

Licensing and regulatory compliance should be your first checkpoint. Verify the title insurance company, agent, or agency holds active Colorado Division of Insurance licensing. Check DORA’s website for licensing status, enforcement actions, or market conduct issues. Licensed providers follow state regulations protecting consumers from fraud and ensuring proper escrow handling.

Service quality and local expertise separate excellent providers from average ones. Companies with proven Colorado market experience understand regional title complications like water rights, mineral rights, and resort area transfer taxes. They process transactions efficiently, respond quickly to questions, and coordinate seamlessly with real estate agents and lenders.

Transparent pricing and fee breakdowns reveal true costs beyond regulated premiums. Request itemized quotes showing title search fees, examination charges, closing services, and endorsement costs. Some companies charge $300 for basic services, while others exceed $800 for identical work. Regulated premium rates stay consistent statewide, but service fees vary significantly and remain negotiable.

Questions to Ask Before Selecting Your Title Company

Start by confirming the company’s licensing status and recent Division of Insurance enforcement history. Request detailed breakdowns of their filed rates, total transaction fees, and which costs are negotiable versus fixed.

Ask specifics about their title search process. How far back do they search property records? What databases and resources do they use beyond county records? Do they physically examine documents or rely solely on digital abstracts? Thorough searches prevent surprises at closing.

Inquire about their post-closing support and claim handling procedures. What happens if title issues surface after closing? Who handles your claim, and what’s their typical response timeline? Strong customer service after closing matters as much as smooth title work before it.

Ask about their technology platforms. Do they offer online portals for tracking your transaction? Can you review documents digitally before closing? Modern title companies streamline processes through technology while maintaining thorough work.

Understanding the Role of Title Companies vs Title Agents

Title insurance companies, called underwriters, assume financial risk and set premium rates filed with Colorado regulators. They create policy forms, handle claims, and maintain reserves to pay covered losses. Major underwriters include Stewart Title, Chicago Title, First American, and Old Republic.

Title agents conduct the actual transaction work under underwriter authority. They perform title searches, issue preliminary commitments, coordinate closings, and manage escrow funds. Agents use the underwriter’s policy forms and rate schedules but compete on service quality, efficiency, and closing fees rather than premium rates.

This distinction matters because agents working for the same underwriter may charge vastly different service fees for identical coverage. Shopping among agents representing your preferred underwriter can save hundreds without sacrificing policy quality. Federal and state laws prohibit anyone from requiring you to use specific title companies, protecting your right to shop independently.

Title Insurance for Different Property Types in Colorado

Different Colorado properties require tailored title insurance approaches based on their unique risk profiles.

Title Insurance for Residential Homes

Residential title insurance follows standardized processes refined through decades of home sales. Lender’s policies are required for financed purchases. Owner’s policies protect your equity against fraud, liens, boundary disputes, and recording errors throughout your ownership.

HOA fees and documents receive priority attention in residential title work. Title companies verify all HOA dues are current and obtain governing documents affecting your property rights. Unpaid HOA assessments must clear before closing since they typically attach as liens against the property.

Standard pre-printed exceptions for easements, covenants, and minor boundary issues appear on most residential commitments. Enhanced policies or specific endorsements can insure over some exceptions for additional premiums, though most residential buyers accept standard exceptions as routine.

Gap coverage remains critical for Colorado’s quick residential closings, preventing claims from slipping through timing gaps between signing documents and completing recording.

Title Insurance for Land Purchases

Vacant land purchases face heightened boundary and survey scrutiny. Without structures marking property lines, disputes arise more frequently over encroachments, access rights, and legal descriptions. Title companies often require current surveys before insuring raw land.

When purchasing land with multiple separate parcels that should function as one property, a contiguity endorsement becomes essential. This covers losses when parcels aren’t actually adjoining due to gaps, intervening parcels, or irregular shapes. This proves particularly relevant for Colorado properties with irregular boundaries or those assembled from multiple purchases over time.

Mineral and water rights create major Colorado land title concerns. Previous owners may have sold subsurface mineral rights separately, giving others legal rights to extract resources below your land. Water rights follow complex appropriation doctrines requiring separate conveyancing formalities. Title policies typically except mineral and water rights unless specifically included through detailed examination.

Limited financing requirements for cash land purchases mean lender’s policies aren’t always necessary. However, owner’s policies remain strongly recommended since raw land ownership claims, boundary disputes, and access issues arise frequently in Colorado’s mix of old homestead patents and modern subdivisions.

Title Insurance for Commercial Properties

Commercial title insurance demands custom underwriting standards reflecting transaction complexity. Enhanced examination protocols account for multiple ownership entities, extensive lien searches across various creditors, and specialized endorsements for lease interests, environmental concerns, and zoning compliance.

Commercial properties often carry multiple lien interests requiring careful priority establishment. First mortgages, second mortgages, mechanic’s liens, judgment liens, and tax liens all compete for position. Title insurance protects against priority disputes by confirming exact lien ordering and insuring against challenges.

Commercial real estate investors benefit from extensive title work that uncovers risks residential buyers rarely face. Environmental liens, historic preservation restrictions, and complicated easement networks demand thorough examination.

Colorado-Specific Title Insurance Considerations

Colorado’s legal landscape and property types create unique title insurance factors that differ from other states.

State Regulations and Requirements

The Colorado Division of Insurance regulates title insurance companies, agents, and premium rates. All providers must hold active licenses verifiable through DORA’s public records. The 2024 Annual Report on Title Insurance shows six closed investigations with no evidence of claims issues, indicating stable market oversight.

Colorado mandates full disclosure of proposed title exceptions in preliminary commitments. Title companies must clearly identify whether they commit to insure over or delete specific exceptions before closing. This transparency requirement helps buyers understand exact coverage limits and negotiate exception removal when possible.

Gap coverage notification became standard practice after regulatory guidance. Colorado title entities must notify insureds that coverage extends to matters recording up to the time your deed officially records at county offices, preventing exposure during critical hours between signing and recording.

Owner’s title insurance disclosure requirements apply to residential transactions. Buyers must receive notice explaining owner’s policy benefits, costs, and optional nature before choosing whether to purchase coverage.

Regional Title Issues Common to Colorado

Water rights complicate Colorado titles more than most states. Appropriation doctrine requires intent to divert, actual diversion, and beneficial use application to establish valid water rights. These rights convey as real property requiring the same formalities as land transfers. Title insurance policies typically except water rights unless specifically examined and included in coverage.

Mineral rights present ongoing challenges, especially in oil and gas producing areas and historic mining regions. Previous owners frequently severed subsurface rights decades ago, giving mineral owners legal authority to access surface land for extraction even without surface owner permission. Title searches identify recorded mineral conveyances, but unrecorded claims remain excluded from standard coverage.

HOA filing irregularities create liens that title searches catch before closing. Colorado law gives HOAs significant lien priority for unpaid dues and assessments. Title companies verify current HOA accounts and require payoffs before insuring. Properties in home inspection processes may reveal HOA issues requiring resolution alongside physical property problems.

Mountain resort area transfer taxes add complexity beyond standard title work. Counties like Pitkin (Aspen) and Eagle (Vail) levy 2% transfer taxes on real estate sales. While these don’t directly affect title insurance premiums, verifying proper tax payment becomes part of the title clearance process.

Title Insurance in Different Colorado Markets

Front Range urban markets like Denver, Boulder, and Colorado Springs benefit from robust county recording systems and experienced title companies. Digital records speed title searches to 3–7 days for most transactions. Competitive title agency markets help buyers shop for the best service fee structures.

Mountain resort markets face unique title challenges. Older property records, complex subdivision histories, and frequent short-term ownership turnover create layered title examination needs. Properties in Aspen, Vail, Telluride, and Crested Butte may require extra search time due to resort-specific complications like timeshare conversions or international owner chains.

Rural plains communities east of I-25 and Western Slope markets work with sparser recording systems. Counties with smaller populations may maintain less comprehensive digital records, requiring examiners to review physical documents. This extends title search timelines by several days compared to Front Range metros.

Agricultural properties across Colorado face distinct title considerations. Farm and ranch lands often include complex water rights, grazing leases, and mineral rights requiring specialized examination. Title companies experienced in agricultural transactions understand these nuances and provide appropriate coverage endorsements for buyers investing in Colorado real estate outside traditional residential sectors.

Enhanced Coverage: When Endorsements Make Sense

Standard title insurance policies contain exceptions that you can insure over through specific endorsements. Understanding when these additional coverages provide value helps you make informed decisions about paying extra premiums.

Survey Coverage and Boundary Endorsements

Survey endorsements protect against errors or discrepancies that might reveal boundary problems or encroachments after purchase. Title companies require additional due diligence (such as current surveys) before issuing these endorsements.

For properties with encroachment risks, several endorsements address specific scenarios. These cover situations where improvements actually sit across property lines or where boundary issues affect described structures. If you’re buying a property where fence lines don’t match legal descriptions or where previous surveys show conflicting boundaries, a survey endorsement’s $250–500 cost proves worthwhile compared to potential $8,000–$15,000 legal fees to resolve disputes.

Colorado-specific endorsements 122.4 through 122.11 handle various encroachment scenarios at different rates. Standard ALTA endorsements 28-06, 28.1-06, 28.2-06, and 28.3-06 also cover encroachments, boundary issues, and easements affecting improvements.

Specialized Property Endorsements

Properties with unique characteristics benefit from specialized coverage. When your insured land contains multiple separate parcels that need to function as one property, contiguity endorsements protect against gaps or irregular shapes that separate parcels. This proves particularly valuable for Colorado properties assembled from multiple purchases or those with irregular boundaries common in mountain regions.

Manufactured housing requires specialized attention. Colorado endorsement 116.5 specifically addresses manufactured housing survey issues, recognizing this property type’s unique title concerns. If you’re purchasing manufactured housing on land you own, this endorsement ensures proper coverage for both the structure and underlying property.

When Title Insurance Claims Become Necessary

Understanding how claims work and what triggers them helps you recognize when to file and what to expect during the process.

Real-World Claim Scenarios

Title insurance claims become necessary when covered defects surface that threaten your ownership or require legal defense. Based on industry data showing $336 million in claims paid through the first half of 2025 alone, these situations occur frequently enough to justify the protection.

Here’s a scenario where a property owner discovers an undisclosed easement after closing. A neighbor claims a recorded easement from 1985 gives them vehicle access across the new owner’s backyard, effectively limiting where the owner can build a planned addition. The title search missed this easement buried in decades-old county records. The owner’s title insurance covers legal fees to challenge or clarify the easement, potentially saving $12,000–$20,000 in attorney costs.

Fraud cases create another common claim type. A homeowner receives notice that someone forged their predecessor’s signature on the deed three owners back, potentially invalidating the entire chain of title. Without title insurance, proving legitimate ownership could cost tens of thousands in quiet title actions. The policy covers both the legal defense and any financial loss if the claim proves valid.

HOA dispute claims arise when associations assert lien priority for assessments the title search failed to uncover. An owner facing a $15,000 HOA lien from previous owners’ unpaid dues files a claim. The title company’s error in missing the lien during examination triggers coverage, with the insurer either paying the lien or defending the owner’s position that it should have been cleared before closing.

Filing a Title Insurance Claim in Colorado

Contact your title insurance underwriter immediately when potential title problems appear. Look for the underwriter name and claims contact information printed on your title insurance policy. Most major underwriters maintain dedicated claims departments with toll-free numbers and online filing portals.

Document the issue thoroughly before filing. Gather copies of your title policy, deed, any notices or legal documents asserting claims against your property, and correspondence related to the problem. Detailed documentation helps claims adjusters understand your situation and process claims efficiently.

Submit your claim in writing even if you’ve spoken with the company by phone. Include your policy number, property address, brief description of the title defect, supporting documents, and contact information.

Most title insurers acknowledge claims within 15 business days and begin investigations immediately. They’ll review your policy coverage, examine the alleged defect, and determine whether your situation falls under covered claims. Claims involving straightforward lien errors may resolve in weeks, while complex ownership disputes can take months or years.

How Title Insurance Companies Handle Disputes

Title insurance companies investigate claims by examining public records, reviewing your policy’s coverage and exceptions, and consulting with legal experts. They determine whether the alleged defect existed before your policy’s effective date and whether your policy’s coverage clauses apply.

For covered claims, insurers provide legal defense at no cost to you. They hire attorneys experienced in title disputes to represent your interests in negotiations, litigation, or quiet title actions. This legal defense benefit alone often justifies title insurance premiums, as real estate litigation costs tens of thousands of dollars.

If claims prove valid and result in ownership loss or impairment, insurers compensate you up to your policy’s coverage limit. Owner’s policies typically cover your full purchase price, though actual settlements depend on the specific loss sustained.

Companies may negotiate settlements before litigation when claims appear legitimate and settlement costs less than trial expenses. They’ll seek your approval before settling claims affecting your ownership rights.

Frequently Asked Questions About Colorado Title Insurance

What is title insurance and do I need it? Title insurance is a one-time premium protecting you from ownership claims tied to past title defects like liens, fraud, or boundary errors. Lender’s policies are required for financed purchases. Owner’s policies are optional but recommended for lifetime equity protection.

What are the two types of title insurance? Owner’s title insurance protects your equity for as long as you own the property. Lender’s title insurance protects the mortgage company’s loan amount, decreasing as you pay down the mortgage.

Who pays title insurance in Colorado? Sellers customarily pay owner’s title insurance as part of their 2.45%–2.47% closing costs. Buyers pay lender’s title insurance since it protects the mortgage company. These customs remain negotiable.

How much does title insurance cost in Colorado? Owner’s policies typically cost 0.5%–1% of the purchase price, roughly $1,000–$2,000 for Colorado’s median-priced homes. Short-term discounts cut costs 55%–75% if recent title insurance exists.

What does title insurance cover? Standard policies cover ownership disputes, hidden liens, fraud, forgery, boundary disputes, recording errors, and undisclosed heirs. Policies exclude zoning issues, environmental hazards, post-purchase liens, and known defects listed in exceptions.

How long does the title insurance process take? Title searches complete in 1–3 weeks depending on property complexity. Issue resolution adds 11–17 days on average. Final policy issuance happens post-closing, taking 18–25 days from initial order through delivery.

Conclusion

Title insurance protects Colorado buyers’ most valuable investment from hidden legal threats that standard inspections never reveal. Understanding coverage types, costs, and the selection process ensures you secure appropriate protection for your property type and transaction structure.

Smart buyers shop multiple licensed Colorado title companies, compare total costs beyond regulated premiums, and verify thorough title search processes before committing. Regional considerations like water rights, mineral rights, and resort area complications require experienced providers who understand Colorado’s unique property landscape. The right title insurance Colorado coverage helps you avoid ownership disputes and hidden liens that can cost far more than the one-time premium.

Ready to secure your Colorado property investment with confidence? Contact JROC Properties at (303) 862-4939 or email rocco@jrocgroup.com to discuss your title insurance needs and connect with top-rated Colorado title companies. Download our comprehensive Buyer’s Guide for step-by-step insights into title insurance and every closing requirement protecting your investment in 2026 and beyond.