Appraisal Gap Meaning: 2026 Buyer’s Guide

Understanding the appraisal gap meaning can save home buyers thousands of dollars and prevent deal-breaking surprises at closing. Whether you’re entering today’s housing market or already under contract, knowing how appraisal gaps work and what to do about them is essential for protecting your investment while keeping competitive offers strong.

Navigating Colorado’s competitive real estate market requires preparation for scenarios like appraisal gaps that can derail transactions. At JROC Properties, we help buyers throughout Boulder County understand these complexities before they become problems, ensuring you enter negotiations with clear expectations and strategic options.

Need Expert Guidance on Your Colorado Home Purchase?

JROC Properties specializes in helping buyers navigate complex scenarios like appraisal gaps in Boulder, Longmont, Lyons, and Denver. Our team brings deep local market knowledge to ensure you’re prepared for every stage of your transaction. Contact us today for a consultation on your home buying strategy.

TL;DR

An appraisal gap occurs when a home’s professional appraisal comes in lower than your agreed purchase price, creating a funding shortfall since lenders base loans on appraised value rather than contract price. In 2024, under-appraisals occurred in 5-8% of transactions nationally, with average gaps of 6-9% below sale price. Your main options include paying the difference in cash, renegotiating with the seller, requesting reconsideration of the appraisal, or walking away if protected by contingencies. Smart buyers set firm gap coverage limits upfront, conduct thorough pre-offer research, and price offers realistically based on comparable sales data. Including an appraisal gap coverage clause can strengthen your offer while maintaining financial boundaries that protect your long-term stability.

Key Points

- Appraisal gaps create immediate cash requirements at closing since lenders only finance up to the appraised value, not the purchase price

- 8.6% of appraisals came in below contract price as of mid-2024, down from 10.7% the prior year as markets cooled

- Buyers can pay the gap in cash, renegotiate price reductions, challenge the appraisal with additional data, or exit via contingencies

- Appraisal gap coverage clauses commit you to covering shortfalls up to a specific dollar amount, making offers more competitive

- Set your maximum gap coverage before making offers, ensuring you maintain reserves for closing costs and emergencies

- Pre-offer comparative market analysis and realistic pricing based on recent sales prevent most gaps before they occur

- Document all home improvements thoroughly and present strong comparable sales data to support appraisals

Table of Contents

What Is an Appraisal Gap?

An appraisal gap represents the financial shortfall between your contract purchase price and the home’s professionally determined appraised value. When you agree to buy a home for $500,000 but the appraiser values it at only $470,000, that $30,000 difference is your appraisal gap. This concept matters because mortgage lenders base their loan amounts strictly on the appraised value, which protects them from financing more than a property’s verified worth.

How Appraisal Gaps Work in Real Estate Transactions

The appraisal process begins after your offer gets accepted. Your lender orders an independent appraisal to confirm the home’s market value. Professional appraisers analyze the property’s condition, location, features, and recent comparable sales to determine an objective valuation. If this appraisal lands below your agreed price, you’re facing immediate decisions about how to bridge that gap.

Lenders calculate your loan based on the lower of two numbers: the purchase price or the appraised value. Take our earlier example. If you planned to put 20% down on that $500,000 home, you expected to finance $400,000. But with a $470,000 appraisal, your lender will only approve $376,000 (80% of the appraised value). You now need to bring an extra $24,000 to closing beyond your original down payment, or find another solution.

Here’s why appraisal gaps create such significant challenges. You’ve already committed to a price through your contract, but your financing just shrunk unexpectedly. The gap forces immediate action, whether that means scrambling for extra cash, reopening negotiations, or potentially losing your earnest money deposit if you can’t proceed.

Why Appraisal Gaps Matter to Buyers and Lenders

For buyers, appraisal gaps introduce sudden financial strain at a vulnerable moment. You may have already paid for inspections, committed to moving dates, or given notice on your current housing. Coming up with thousands of additional dollars on short notice can derail your purchase entirely or force difficult financial compromises.

Understanding typical closing costs in Colorado helps you budget for unexpected expenses like appraisal gaps, ensuring you maintain adequate reserves throughout the transaction.

Lenders view appraisals as essential risk management. They need assurance that if you default and they foreclose, the property’s sale will recover their loan amount. An appraisal lower than the purchase price signals that you might be overpaying, which increases the lender’s exposure. This protection benefits buyers too, even when it feels frustrating, since it prevents you from borrowing more than the home can support.

Market dynamics in 2024 showed interesting patterns. While 57% of appraisals exceeded sale prices in the second half of the year with an average over-appraisal of 4%, under-appraisals still occurred frequently enough to require buyer preparation. The frequency of under-appraisals dropped to 8% from 12% a year earlier, reflecting cooling market conditions where prices aligned more closely with valuations.

What Causes an Appraisal Gap?

Several market forces and property-specific factors contribute to appraisal gaps. They often work together to create valuation mismatches. Understanding these causes helps buyers anticipate risk before making offers.

Competitive Market Conditions and Pricing Expectations

When markets transition from seller-driven to balanced conditions, list prices may reflect prior high-demand periods while appraisals rely on current closed sales. Sellers who remember peak valuations from six months earlier may resist adjusting expectations. This creates a disconnect between asking prices and objective current values.

This gap intensifies when sellers price homes based on emotional attachment or limited market knowledge rather than recent comparable sales. A homeowner who invested heavily in custom features may expect those improvements to translate dollar-for-dollar into higher value. But appraisers assess what typical buyers actually pay for such features in that specific market.

Risk varies by property type and location. Unique properties in neighborhoods with limited recent sales activity create challenges for appraisers who must make larger adjustments to dissimilar comparables, potentially resulting in conservative valuations that disappoint sellers who priced at the high end.

Property-Specific Issues That Lower Appraised Value

A home’s physical condition directly impacts its appraised value. Structural problems like foundation cracks, roof damage, or outdated systems such as aging HVAC, plumbing, or electrical components substantially reduce valuations. Pest infestations, particularly termites, also trigger significant downward adjustments that may not be apparent during initial viewings.

Being aware of home inspection red flags before making an offer helps you anticipate potential appraisal issues related to property condition.

Unique or highly customized properties present special challenges. Features that appeal to specific buyers, such as elaborate landscaping or specialized rooms, may not add proportional value in an appraiser’s analysis. Properties with unusual architecture lack sufficient comparable sales, forcing appraisers to make less precise value estimates that can skew conservative.

Buyers sometimes overlook maintenance issues when falling in love with a home’s potential. That dated kitchen you planned to renovate affects the current appraisal even if you see it as an opportunity. Appraisers assess the property’s present condition, not its future state after your improvements.

Comparable Sales Data Limitations

Appraisers depend heavily on recent comparable sales, typically within the past three to six months and within a mile of the subject property. When suitable comps are scarce, as in neighborhoods with few recent transactions or for unusual properties, appraisers must stretch these parameters or make larger adjustments to dissimilar properties.

Market timing also matters. If you’re buying in a rapidly appreciating neighborhood, the appraiser’s comps from three months ago may not reflect current values. In cooling markets where inventory is rising, recent comps might show declining trends that pull your appraisal below an offer price set weeks earlier.

According to Fannie Mae research, collateral-related loan defect rates differ by only 0.6% between traditional appraisals and those using property data collections, suggesting appraisals are generally reliable when appraisers have access to appropriate data. However, legitimate valuation challenges occur when comparable sales are scarce or property features are truly unique.

Your Options When Facing an Appraisal Gap

Discovering an appraisal gap triggers immediate decision-making. Each option carries different financial implications and strategic considerations for your purchase.

Pay the Difference in Cash

The most straightforward solution involves bringing extra cash to closing to cover the gap. If the home appraises $20,000 low, you write a check for that additional amount on top of your planned down payment and closing costs. This approach keeps the deal moving forward without requiring seller cooperation.

This option works best when gaps are relatively small and you have accessible reserves. Before committing, calculate whether covering the gap leaves you with adequate emergency funds. Most financial advisors recommend maintaining three to six months of expenses after closing, accounting for not just the gap but also moving costs and immediate home needs.

Consider the property’s true value carefully. Paying a gap means accepting that you’re spending more than the appraiser believes the home is worth. While this might make sense in neighborhoods with strong appreciation trends or unique properties where comps are imperfect, it carries risk if you’re overpaying in a declining market.

Renegotiate the Purchase Price with the Seller

Opening negotiations after a low appraisal provides objective evidence for a price reduction. Sellers often respond to appraisals more receptively than to initial buyer offers, since the valuation comes from an independent professional rather than an interested party.

Your negotiating leverage depends on market conditions and seller motivation. In balanced markets where inventory is healthy and days on market are extended, sellers may prefer accepting a price reduction over relisting and waiting months for another buyer who’ll face the same appraisal challenge.

Common outcomes include splitting the difference, where you cover half the gap in cash while the seller reduces their price by the other half. This compromise maintains goodwill while acknowledging the appraisal’s message. Your agent’s skill in framing this conversation matters enormously, presenting appraisal data persuasively while preserving deal momentum.

Working with Local Market Experts Makes All the Difference

JROC Properties’ deep knowledge of Boulder County’s real estate landscape helps buyers navigate appraisal negotiations successfully. We understand local appraiser patterns and know how to present compelling cases for value reconsideration. Reach out to our team to discuss your specific situation.

Request Reconsideration or Challenge the Results

If you believe the appraisal contains errors or overlooks important factors, you can request a reconsideration of value. This involves providing your lender with additional documentation such as comps the appraiser may have missed, records of recent improvements with permits and receipts, or corrections to factual errors like incorrect square footage.

The reconsideration process adds time to your transaction, typically one to two weeks. You’ll need to gather compelling evidence and your lender must agree the challenge has merit. Success happens most often when you identify clear factual mistakes or provide truly comparable sales the appraiser didn’t access.

Documented evidence of recent home renovations in Colorado can support appraisal reconsideration requests, especially when improvements add measurable value that comps don’t reflect.

Some buyers opt for a second full appraisal, though this requires lender approval and additional cost. The second opinion only helps if it comes in higher, and there’s no guarantee. Most lenders will average two appraisals if both are ordered, which might not fully solve your gap.

Walk Away from the Deal

Your appraisal contingency, if included in your contract, protects your right to cancel the purchase if the appraisal comes in low. You receive your earnest money deposit back and avoid forcing a purchase that doesn’t align with market value. This option makes sense when the gap is substantial, you lack the cash to cover it, and the seller won’t negotiate.

Walking away feels difficult after the emotional investment of finding your dream home, but it’s sometimes the smartest financial decision. If you’re stretching to buy a $600,000 home that appraises at $550,000, covering that $50,000 gap might leave you house-poor and financially vulnerable. Future you will appreciate the restraint.

The fear of missing out shouldn’t drive you to financial overextension. If this deal doesn’t work, others will emerge. Market conditions fluctuate, and patience often rewards buyers with better opportunities.

Appraisal Gap Coverage: Clauses and Contingencies Explained

Understanding the contractual tools that address appraisal gaps helps you structure competitive offers while maintaining appropriate protections.

What Is an Appraisal Gap Coverage Clause?

An appraisal gap coverage clause is a provision in your purchase agreement where you commit to covering the difference between the purchase price and appraised value up to a specified dollar amount. For example, your offer might state: “Buyer agrees to cover up to $25,000 above the appraised value, but not to exceed the purchase price.”

This clause signals to sellers that you’re financially prepared and committed to closing even if the appraisal disappoints. In competitive situations, it can differentiate your offer from others that rely entirely on appraisal contingencies. Sellers appreciate knowing they won’t face renegotiations or deal collapses over reasonable appraisal shortfalls.

The clause should specify your maximum exposure clearly. Never commit to covering unlimited gaps, which could expose you to catastrophic costs if the appraisal comes in drastically low. Your limit should reflect your genuine financial capacity while leaving adequate reserves for closing costs, moving, and post-purchase needs.

Appraisal Contingency vs. Appraisal Gap Coverage

These two provisions serve different purposes and aren’t mutually exclusive. An appraisal contingency allows you to walk away from the deal without penalty if the home appraises below the purchase price, protecting your earnest money deposit. It gives you an exit if you can’t or won’t cover the gap.

Appraisal gap coverage commits you to proceeding with the purchase by covering a defined shortfall. You’re giving up your right to exit for gaps within your stated limit. This commitment makes your offer stronger but reduces your flexibility.

Many buyers use both provisions together strategically. You might cover gaps up to $20,000 but retain your contingency for gaps beyond that amount. This structure reassures sellers you’ll handle moderate shortfalls while protecting you from massive appraisal problems. The combination balances competitiveness with prudent risk management.

How to Structure Appraisal Gap Coverage in Your Offer

Crafting effective gap coverage requires understanding your financial position and market dynamics. Start by reviewing your complete financial picture: available cash, reserve requirements, typical closing costs (1-3% of purchase price in most markets), and post-closing needs.

Calculate your true maximum by working backward from your total liquid assets. If you have $80,000 in savings and a $550,000 purchase requiring $110,000 down (20%) plus $11,000 closing costs leaves $41,000. Subtract a safety buffer of $15,000 for moving and emergencies, giving you $26,000 available for gap coverage. Consider offering to cover up to $20,000, leaving additional cushion for surprises.

Your agent should present gap coverage as confidence rather than desperation. Frame it as “Buyer has strong financial reserves and will cover up to [amount] to ensure closing” rather than suggesting you’ll pay any price. Moderate gap coverage is competitive without being excessive in most current market conditions.

Property-specific factors matter when setting limits. Homes with unique features, limited comps, or in rapidly appreciating neighborhoods might justify higher coverage commitments. Properties in established neighborhoods with abundant recent sales carry lower appraisal risk, requiring less coverage to compete effectively.

Deciding How Much Appraisal Gap to Cover

Setting your gap coverage limit demands honest assessment of both your financial capacity and the property’s realistic value.

Assessing Your Financial Capacity

Begin with a complete inventory of your liquid assets: savings accounts, easily accessible investments, and any family gifts designated for your purchase. Subtract your required down payment, estimated closing costs, and mandatory reserves. What remains represents your theoretical maximum gap coverage.

Apply conservative buffers to this calculation. Real estate transactions generate unexpected costs, from last-minute repairs to higher-than-quoted moving expenses. Buying a home also reveals immediate needs like window treatments, minor repairs, or essential furnishings. Plan for these realities rather than arriving at closing with zero cushion.

Working with JROC Properties’ preferred lenders ensures you understand your complete financial picture and can structure gap coverage that maintains healthy reserves throughout the transaction.

Your debt-to-income ratio deserves attention, particularly if you’re already pushing lender limits. Adding significant gap coverage might not affect your approved loan amount, but it reduces your liquid reserves at exactly the moment you’re taking on substantial new financial obligations. Most advisors recommend maintaining six months of mortgage payments in accessible savings after closing.

Remember that covering an appraisal gap means accepting that you’re paying more than the professional valuation. If financial stress would result, reconsider whether this purchase serves your long-term interests.

Evaluating the Property’s True Value and Market Position

Independent research beyond the listing price reveals whether gap coverage makes strategic sense. Analyze recent comparable sales yourself using public records or real estate platforms. Look for similar properties in condition, size, location, and features that sold within the past three months.

If comps support the listing price or higher, modest gap coverage protects against conservative appraisers while buying into legitimate value. But if recent sales run 5-10% below your offer price, gap coverage might be funding an overpayment you’ll regret.

Consider appreciation trends in the specific neighborhood. Areas with consistent 3-5% annual growth might justify covering a gap to secure a property in an appreciating market. Neighborhoods with stagnant or declining values make gap coverage riskier, since you’re betting against current market signals.

Property condition matters enormously. Homes in excellent condition with updated systems appraise more reliably than fixer-uppers. If you’re buying a property with deferred maintenance or obvious issues, expect lower appraisals and limit your gap commitment accordingly.

When to Limit or Avoid Gap Coverage Commitments

Several scenarios call for minimal or no gap coverage commitments. If you’re buying at the absolute top of your budget, additional cash requirements create genuine financial hardship. When your down payment exhausts most liquid savings, promising to cover gaps you realistically can’t fund is irresponsible.

Properties in declining markets or with significant condition issues don’t warrant substantial gap coverage. If neighborhood sales show consistent downward trends, covering gaps means fighting market reality.

First-time buyers with limited reserves should prioritize maintaining emergency funds over aggressive gap coverage. Your financial security matters more than winning any single property. Markets fluctuate, and other opportunities will emerge at more favorable terms.

Sometimes offering no gap coverage is strategically sound. If your research suggests the listing price already exceeds market value, let your appraisal contingency protect you. Sellers testing the high end of pricing should bear the risk of appraisal gaps, not buyers.

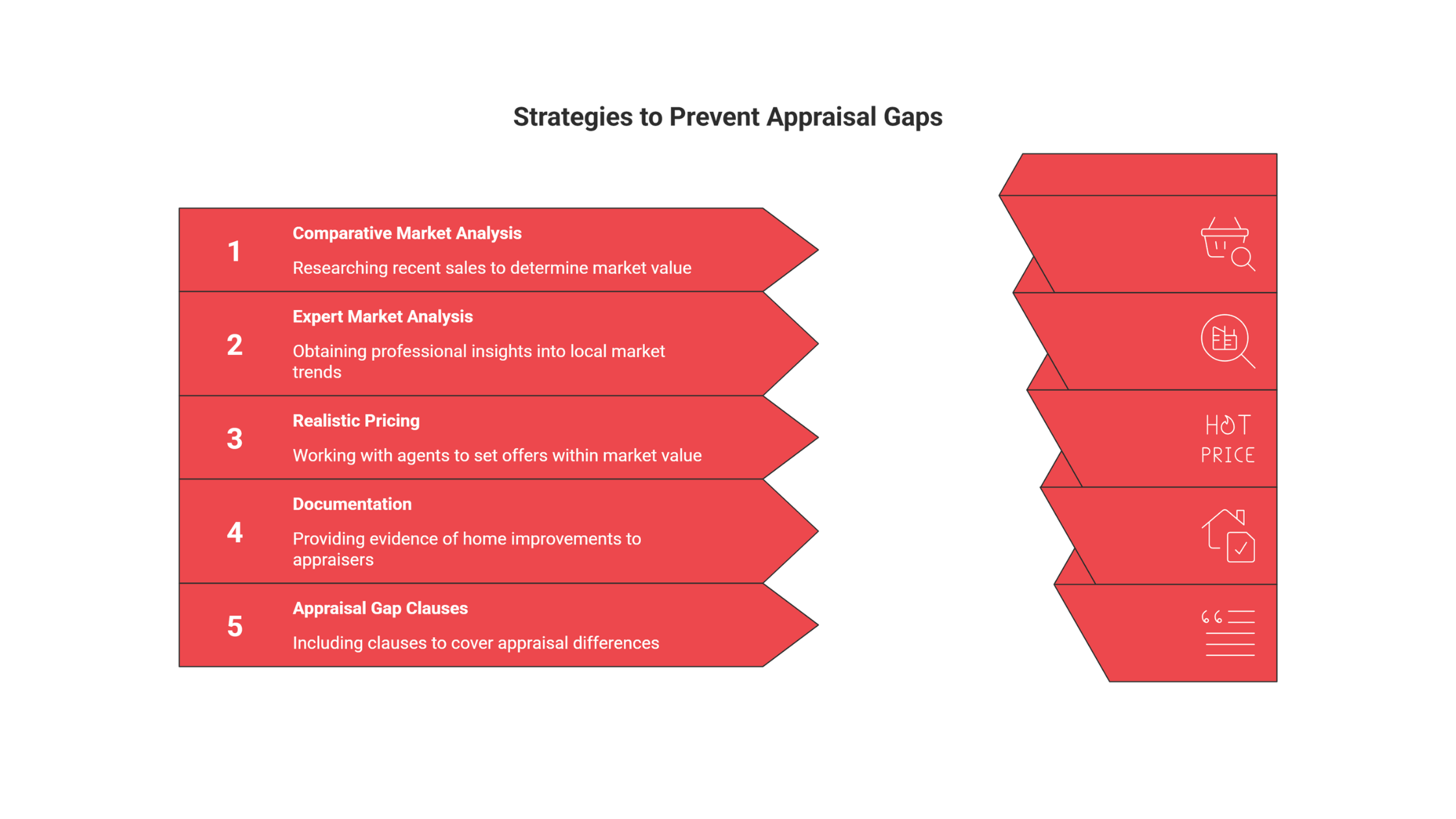

Top Strategies to Prevent or Minimize Appraisal Gaps

Proactive planning prevents most appraisal gaps before they occur. These strategies position you for successful transactions without surprises.

Conduct Thorough Comparative Market Analysis Before Offering

Research comparable sales meticulously before making offers. Identify at least five similar properties that sold within the past three months and within one mile. Adjust for differences in size, condition, updates, and lot features. This analysis reveals realistic market value and flags potentially overpriced listings.

Top brokerages instruct agents to run detailed comps on target properties, avoiding bids significantly above market value by staying within 5-10% of recent sales. When your offer aligns with recent comps, appraisals typically confirm your pricing.

Get Expert Market Analysis for Your Target Property

JROC Properties provides detailed comparative market analysis for buyers throughout Boulder County, helping you make informed offers that align with true market value. Our local expertise in Boulder, Longmont, Lyons, and Denver ensures you understand neighborhood-specific pricing patterns. Schedule your consultation today.

Work Closely with Your Agent to Price Offers Realistically

Experienced agents understand local appraisal patterns and appraiser tendencies. They know which improvements add value and which don’t translate to higher appraisals. Trust their guidance when they suggest offering below listing price on overpriced properties or caution against bidding wars that push prices beyond supportable levels.

JROC Properties’ agents bring decades of combined experience in Boulder County real estate, understanding the nuances that affect property valuations across different neighborhoods and price points.

Provide Robust Documentation to Appraisers

When making offers on homes with recent updates, gather documentation of improvements including permits, receipts, dates, and contractor information. Brokerages prepare packets with invoices, before/after photos, warranties, and detailed upgrade descriptions before the appraisal to ensure appraisers account for value-adding improvements often overlooked. Provide this through your lender, ensuring appraisers see documented work like new roofs, HVAC systems, or kitchen renovations that substantially boost valuations.

Include Strategic Appraisal Gap Clauses in Offers

Buyers who commit upfront to cover a specific dollar amount (typically $10,000-$15,000) above the appraised value strengthen offers in competitive markets by addressing seller concerns while maintaining defined financial limits. Draft the clause in the purchase agreement, capping your exposure while reassuring sellers the deal won’t collapse over moderate valuation differences. This balanced alternative to waiving contingencies entirely gives you an edge over purely contingent bids.

Understand Escalation Clause Risks

Escalation clauses automatically increase your offer above competing bids up to a maximum price. While they win bidding wars, they also push prices beyond recent comps, creating appraisal gap risk. Escalation clauses can cause offered prices to exceed appraised values, requiring buyers to cover differences in cash. Use escalation clauses cautiously and pair them with gap coverage limits that reflect your true financial capacity.

Real-World Appraisal Gap Examples

Note: The following scenarios are composites based on actual transaction patterns with details modified to protect client privacy while illustrating typical outcomes.

Scenario 1: Covering a Small Gap After Competitive Bidding

After finding a well-maintained home in a desirable suburban neighborhood listed at $825,000, a buyer faced multiple competing offers. She bid $850,000 with $20,000 appraisal gap coverage after research showed recent comparable sales supported $835,000-$845,000, making her offer defensible but aggressive.

The appraisal came in at $840,000, creating a $10,000 gap well within her committed coverage. Her lender approved a loan based on the $840,000 appraised value, reducing her mortgage by $8,000 (at 80% LTV) from her planned financing. She brought an extra $10,000 to closing as promised, which increased her equity position slightly versus her initial plan.

This scenario worked because the buyer had researched values thoroughly, understood the comp support, and structured gap coverage she could genuinely afford. She secured a home in a desirable, historically appreciating neighborhood where the $10,000 premium felt reasonable given her long-term outlook.

Scenario 2: Negotiating Down After a Significant Gap

A couple offered $575,000 on a property listed at $565,000, adding $10,000 above asking in a competitive situation. They included $15,000 gap coverage but maintained their appraisal contingency for larger shortfalls. When the appraisal returned at $540,000, they faced a $35,000 gap exceeding their commitment.

Their agent immediately opened negotiations, presenting the appraisal to the sellers with a proposal: buyers would cover their committed $15,000, sellers would reduce price by $15,000, meeting at $560,000. This approach split the unexpected difference while honoring their contractual gap coverage.

The sellers initially resisted but faced reality after discussing the situation with their agent. Any future buyer would encounter the same appraisal, and relisting meant months of additional carrying costs in a market with rising inventory. After two days of negotiation, they accepted the compromise, and the deal closed.

This example demonstrates the power of reasonable gap coverage paired with strong contingency protection. The buyers showed good faith through their commitment while preserving leverage for larger problems. Skilled negotiation framing this as cooperative problem-solving rather than adversarial preserved goodwill and achieved a fair outcome.

Scenario 3: Walking Away When Numbers Don’t Work

A buyer bid $680,000 on a property with minimal gap coverage ($5,000) and a strong appraisal contingency. His inspection revealed aging systems needing replacement within 3-5 years, which concerned him but didn’t derail the purchase. The appraisal at $635,000, however, created a $45,000 gap he couldn’t and wouldn’t cover.

His financial analysis showed covering even half the gap would deplete his reserves dangerously, leaving nothing for the system replacements his inspection identified. He requested the seller reduce the price to $640,000 (splitting the difference), but the seller refused, insisting the appraisal was flawed due to unique property features.

After careful consideration of market conditions and realistic expectations, the buyer invoked his appraisal contingency and walked away with his earnest money intact. Three months later, he purchased a different property for $625,000 that appraised at contract price and required fewer near-term repairs. His patience and financial discipline prevented overextension that would have caused stress for years.

This scenario reinforces that walking away is sometimes the smartest move. The buyer avoided both financial overextension and a property with condition issues at an inflated price. In shifting markets, patience often rewards buyers with better opportunities.

Navigating Appraisal Gaps in Today’s Housing Market

Current market dynamics present distinct considerations for appraisal gap management. Understanding these conditions helps you strategize effectively.

National data from 2024 provides useful benchmarks. Under-appraisal frequency dropped to 8% in the second half of 2024 from 12% a year earlier, with average under-appraisals improving to 6% below sale price from 8%. Simultaneously, 57% of appraisals exceeded sale prices with an average over-appraisal of 4%, suggesting markets were generally supporting or exceeding agreed prices as conditions cooled.

Regional variations matter significantly. Data across 19 states showed under-appraisal frequencies ranging from 3% to 14% depending on local market dynamics. Markets with rapid price appreciation or limited inventory showed different patterns than those with abundant supply and stable pricing.

Understanding Colorado’s real estate market trends helps you anticipate whether appraisal gaps are likely in your target neighborhoods and price ranges.

The relationship between mortgage rates and appraisals deserves attention. With rates remaining elevated compared to the ultra-low environment of 2020-2021, buyer purchasing power remains constrained. Appraisers factor prevailing rates into their calculations, as higher financing costs reduce how much buyers can pay. This rate environment supports more conservative appraisals that align with actual market conditions rather than aspirational pricing.

Position yourself strategically by maintaining strong financial reserves, conducting thorough due diligence, and working with experienced local agents who understand your market’s micro-dynamics. Different neighborhoods and property types carry varying gap risks (urban condos face different dynamics than suburban homes or rural properties).

The key is balancing competitiveness with prudence. Offering moderate gap coverage shows sellers you’re serious while maintaining contingencies for larger problems. In many current markets, this balanced approach wins deals without forcing financial overextension.

Conclusion

Appraisal gaps require careful navigation, but understanding your options and setting clear boundaries protects your financial future while maintaining competitive positioning. The appraisal gap meaning extends beyond simple definitions to real financial implications that affect both your immediate closing and long-term equity.

Smart buyers should establish maximum gap coverage before house hunting, ensuring any commitment leaves adequate reserves for closing costs, moving, and emergencies. Research comparable sales thoroughly to identify realistic property values, avoiding overpayment in enthusiasm. Include gap coverage clauses strategically to strengthen offers while maintaining contingencies for significant shortfalls.

When gaps emerge, evaluate each situation independently based on the property’s true value, your financial capacity, and market conditions. Negotiate confidently using the appraisal as objective evidence, and don’t hesitate to walk away when numbers don’t support proceeding. In many markets, improving inventory and buyer leverage mean other opportunities will emerge.

Whether you’re a first-time buyer or experienced investor, understanding appraisal gaps positions you for successful transactions in Colorado’s dynamic real estate market.

At JROC Properties, we specialize in guiding buyers through complex scenarios like appraisal gaps throughout Boulder County. Our team brings deep knowledge of local market conditions, appraiser patterns, and negotiation strategies that protect your interests while keeping deals on track. Founded by Jami and Rocco Montana, JROC Properties combines strategic insight with personalized service, ensuring you understand every option before making irreversible commitments.

Understanding what is an appraisal gap and how to handle it transforms a potentially stressful surprise into a manageable challenge. With preparation, research, and expert guidance, you’ll navigate real estate markets successfully while maintaining the financial stability that makes homeownership rewarding rather than stressful.

Don’t let appraisal gaps derail your Colorado home buying journey. JROC Properties provides expert guidance throughout Boulder, Longmont, Lyons, and Denver, helping you structure competitive offers while protecting your financial interests. Our local market expertise and client-first approach ensure you’re prepared for every scenario.